As doubts grow that in the post Dubai world Russia’s central bank will be able to sustain a great deal of momentum in its ongoing programme of interest rate reductions, we learn this week that the pace of expansion in Russia’s economy slowed back in November, following two months of steady advance in September and October. This time services activity also weakened its advance while manufacturing activity registered its second month of contraction. Yet the central bank may well show increasing restraint in lowering interest rates, even as the economy slows, the ruble rises, and bank retail lending continues to fall, having declined for nine consecutive months up to and including October, while corporate lending dropped for a second month in a row and hasn’t risen for six months (for more on the particular topic see my recent post – Are Russia’s Consumers Getting “Carried Away” With Themselves?). Continue reading

Author Archives: Edward Hugh

Global Manufacturing Loses Momentum In November

Operating conditions in global manufacturing industry improved for the fifth successive month in November, although there was an evident slowdown in the overall rate of expansion, with differences between countries accentuating and not diminishing. The JPMorgan Global Manufacturing PMI aggregate reading came in at 53.6, down from October’s 39-month high of 54.4, and signalling that the first wave of post crisis momentum may be losing force as governments slowly start to remove stimulus measures.

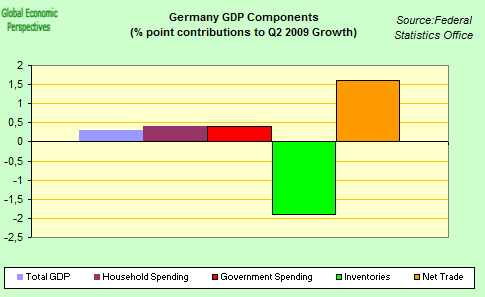

Is There A Double Dip Risk In Germany?

This is not an idle question. Despite all those bullish headlines in the press, most informed observers – including Bundesbank head Axel Weber – are only to well aware of just how fragile the German recovery actually is. Indeed only last week the OECD warned that Germany’s economy, may only recover slowly next since investment “is lagging,â€. The OECD now predict that German gross domestic product will expand 1.4 percent in 2010 and 1.9 percent in 2011 after shrinking 4.9 percent this year, which is in fact up on their earlier estimate, where the OECD predicted German growth of 0.2 percent next year. So whichever way you look at it, output at the end of 2010 will still be well down of 2008 levels. Worse, events like the recent upheaval in Dubai start to cast doubts on whether even the rather optimistic 1.4 percent growth level may now not be excessively optimistic for next year. The problem is that the recent rebound in Eurozone growth is extremely uneven as between countries, and, given its long standing export dependence, the German economy is hardly going to be leading the charge. As I said in my most recent post on the Eurozone :

“The question in hand is the Eurozone third quarter growth one, and the story is all about differences (between countries) and these differences in the key cases (France and Germany) are in many ways all about inventories……Now if you look at the chart below, you will see that German growth was in the second quarter was, more than anything, a statistical quirk which resulted from a balancing act between strong swings in inventories and in net trade. In the third quarter, as far as we can see (since we don’t have that ever so important detailed breakdown), this position has quite literally been inverted, as the earlier trade bonus has been eaten away by growth in imports (largely to stock up on export oriented inventories, not items destined towards domestic consumption) and this part we more or less know, since we do have all the trade data in for the quarter. ”

Total Eclipse At The Heart Of Dubai’s World

Back in the heady days of 2006 some 30,000 cranes, roughly a quarter of total global capacity, were busy whirring away in Dubai. Today most of these devices have either left to find service in other parts of the globe, or lie silent, unused and unloved. In what is only the latest sign of the ongoing property snarl-up affecting the emirate Nakheel, Dubai World’s property developer subsidiary, asked on Wednesday for a delay in their next debt payment. The move was widely seen by investors as a technical default, raising concerns about investment in risky assets right across the globe. So while their company slogan may well be that the sun never sets over Dubai World, the fact is that Dubai World’s sun not only no longer shines, it is suffering from something more like a total eclipse. Continue reading

Are Russia’s Consumers Getting “Carried Away” With Themselves?

“Cutting rates by 50 basis points here and there is not going really diminish the appeal of the ruble,†said Manik Narain, an emerging markets strategist at Standard Chartered Bank Plc in London. “In terms of nominal interest rates Russia (at 9% as of 24 November) is still offering the highest yields in the emerging market space and in an environment where oil prices are remaining relatively well supported we think that the ruble will continue to be seen as an attractive way to position for global recovery,â€

The world’s central banks are having a hard time of it these days, having just gotten through the worst banking and financial crisis in living memory they now face a growing dilema between continuing to give support to the developed economies (which are yet to recover from those early hammer blows) and the danger of creating fresh global asset price bubbles in emerging economies, asset bubbles which could easily be being fuelled by low US interest rates and a weak dollar. The latest warning in this respect comes not from Nouriel Roubini (or even from me, but see this post, and this recent interview I gave on Forex Blog), rather it emmanates from Germany’s new finance minister, Wolfgang Schäuble. His comments – which were cited in last Saturday’s Financial Times – highlight official concern in Europe that the exceptional steps taken by central banks and governments to combat the crisis carry with them a series of undesireable side effects. Continue reading

Just How Much Of A Eurozone Rebound Really Was There In Q3?

Sorry, and I apologise in advance: in this post I’m going to be a nit-picker. The question in hand is the Eurozone third quarter growth one, and the story is all about differences (between countries) and these differences in the key cases (France and Germany) are in many ways all about inventories. So maybe I should have titled the post “all about inventories”, following Pedro Almodovar’s cinematographic lead in cycling and recycling that old “all about Eve” metaphor – necessity is the mother of invention, and movements in inventories are progenitors of both growth, and of that notorious double dip difficulty. So just which one of these is it that we have on our hands here? Continue reading

The Dollar As A Funding Currency

Nouriel Robini is not a man who is known for mincing his words. “We have the mother of all carry trades,†he tells us, “Everybody’s playing the same game and this game is becoming dangerous.†There is a “wall of liquidity†sweeping the planet, pushing asset prices ever higher in one country after another. I wholeheartedly agree. Continue reading

Norwegian Wood

Well, if John Lennon had still been around today he would undoubtedly have entitled his song Norwegian oil, but whatever way you want to put it Norway is back in the news, and this time not because of adolescents who find themselves with no alternative to sleeping overnight in the bath-tub, but rather because its central bank has been put in a position where it has little alternative but to raise interest rates, even if in fact it would be more comfortable for it not to do so. So, not being in the habit of looking for a quiet life, decision makers over at the Norges Bank decided last week to put themselves in the hot seat by lifting the banks main rate by 25 basis points to 1.5 per cent and in this inauspicious and modest way entered the history books as the first European central bank to raise interest rates since the financial crisis started to ease. Continue reading

Global Manufacturing, France Outperforms, As Spain Continues To Flounder

Well, it is not as if I relish rubbing salt into old wounds, but this quote from the latest piece by Ben Hall in Paris and Ralph Atkins in today’s Financial Times is just too good to resist.

French manufacturing output rose at its fastest rate for nine years, according to a survey on Monday, confirming that France has become the economic powerhouse of continental Europe. Purchasing managers’ indices for manufacturing showed France performing significantly better than the continent’s other main economies – thanks to robust domestic demand.

Plenty of food for thought in this paragraph it seems to me. As foreshadowed in this earlier post, it is the French economy – and not the German one – which is rebounding sharply, and this seems to be for essentially three reasons:

i) there is still life in domestic demand, due to the fact that demographics are good, and lending to households (at an average rate of increase of 11%) was a lot less during the last boom than it was in the bubble societies (20% per annum in Spain and Ireland

ii) France’s more favourable demography means that the French government has more space for fiscal stimulus (when compared with Germany) which means the “cash for clunkers” can roll on a bit longer.

iii) the combination of these above two factors means that stimulus actually can work, since it can fire up domestic consumption which is not already dead on its feet. That is, the situation is a win-win one in the classic sense (although, as I was arguing at the end of last week, the ECB will now need to do some pretty adroit monetary footwork if it wants to avoid firing up an asset bubble in France, to follow hot on the heels of the one which has just deflated in Spain.

As Jack Kennedy, economist at PMI survey organisers Markit put it:

“The strong recovery in French manufacturing continued in October, with output rising at the fastest pace for nine years. While some of the current strength reflects a rebound from the extreme financial crisis, it nevertheless offers further evidence that the France is towards the front of the pack among developed economies in emerging from the downturn. Domestic demand remains the key driver of growth as confidence continues to recover.â€

A New Spectre Is Haunting Europe, A Spanish One

A spectre is haunting Europe, but this time it is not the spectre of revolt by the popular masses, or even one of yet another wave of bank bailouts. No, the spectre which is currently stalking the corridors of Europe’s most prestigous institutions is one of a Spanish economy which stays on a flatline while Europe’s other economies, one by one, start to struggle back to life. And the main reason that this particular ghostly image is giving everyone so many sleepless nights is because Europe’s current institutional structures, and especially the monetary policy tools available at the ECB are scarcely prepared for such a nighmare eventuality. Continue reading