The Greek tragedy in several acts would appear to be approaching a climactic moment. The warnings coming out of Berlin all week have been hard to ignore: “Greece either puts up or shoves off” would seem to be the blunt message being offered. Continue reading

Category Archives: Economics: Currencies

It’s the geography, stupid

Central and Eastern European economies aren’t doing well. German IFO business confidence tanks, on expectations of poor export orders. These two facts are related.

It’s been said before that the central core of economics failed to predict the great recession (or damn, can’t we call it a depression already? It’s been four years and it’s depressing enough) and that only a few key groups of people noticed anything unusual. Followers of Hyman Minsky and Charles Kindleberger saw the classic pattern of confidence, mania, panic, and crash unfolding. People who understood the economy as a system of accounts saw a number of huge imbalances in the flow of funds. Marxists considered that the source of the imbalances was the super-exploitation of Chinese workers and the maldistribution of the proceeds of growth in the West.

But I’m not sure if economic geography has been given enough credit. One economic geographer who predicted the crisis is of course Paul Krugman. From a geographical perspective, the CEE economies are part of a huge automotive engineering cluster rather like the US rustbelt or the West Midlands in the UK, reaching over from the Cologne area to Slovakia. (Actually, they always have been since the Industrial Revolution – here’s a beautiful 1938 Tatra and a much less beautiful 1914 Skoda 305mm mortar and caterpillar tractor.) From an industrial economics perspective, they are part of the German motor industry’s global supply chain, whether as upstream suppliers of parts and sub-assemblies or as downstream final assembly contractors. You can argue whether geography or functional specialisation determines this, but that’s not really relevant right now.

To put it another way, they aren’t exporters to “the German locomotive” but rather to the German economy’s customers, at one remove. The determining factor of their order books is how well the final products sell, and in the German economy’s historical default state as an industrial exporter, that depends on somebody somewhere buying more German goods than they sell goods to Germany.

A deflationary adjustment of the eurozone trade balances will be deflationary all the way along the supply chains. This is broadly what I was worrying about in May, 2010. The problem is not quite the same as it was for Keynes in the original Economic Consequences, a book which contains a lot of economic geography – back then, if the Germans were ever going to pay off their debts, Keynes pointed out, the rest of Europe had to let them export enough stuff. Now the boot is on the other foot. If the Greeks are ever going to get out of their debt crisis, the Germans have to let them export enough stuff. And if the Czechs and Hungarians and Baltics are not going to slide back into the mud, the Germans have to import enough stuff from them. Nobody imagines that the Greeks will be importing as many BMWs as they used to, so what can the answer be?

Life On PMI Cold Comfort Farm.

As the heat wave which has been hanging over Southern Europe for the last couple of weeks steadily eases off there is little sign that any of the warm air which is disippating is reaching the chilled motors of the European and Chinese economies. The results of this months flash PMI readings are at best more of the same, and at worst show continuing deterioration. While current conditions stabilised in some areas, new orders, and especially new export orders often hit new post-recovery lows. There is every likelihood that the final August global readings will be much more of the same. Continue reading

The Policymaker’s Fear Of The Italian Penalty Shot

“While the impact of service-sector liberalization and privatizations may be positive on medium-term growth, the budget cuts are likely to have quite negative effects on the short-term GDP dynamic. We expect Italian GDP growth to slow to close to zero in 2012 and 2013.†Giada Giani, Citigroup

According to one anonymous German official speaking off the record to reporters from Der Spiegel, “a country like Italy can’t be saved”. We will have to trust that he was referring to the country’s size when he made the statement, and not its existential core. If he was, he may well be right, at least under the Euro Area’s current institutional arrangements. Let’s take a quick look at why. Continue reading

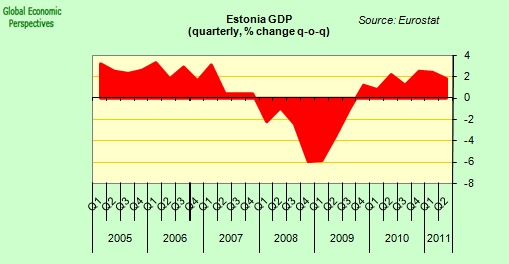

Is The Risk Accompanying Estonia’s Eurozone Membership Really So Low?

“But the go-ahead Estonians are already scenting the next challenge. Should the single currency crumble, they are determined to be on the inside track for any new German-centred “super-euroâ€. Goodbye “eastern Europeâ€; welcome to the “new northâ€.”

Edward Lucas, writing in The Economist

Estonia’s economy put in another sterling performance in the second quarter of this year, even if the expansion rate fell back to quarterly 1.8%, down from 2.4% in Q1, and 2.5% in the last quarter of 2010. Well, you didn’t expect the economy to keep growing at such strong rates for ever, did you? Evidently not. The interannual rate peaked at 8.5% in the first quarter, and dropped back slightly during the last three months to 8.4%, still this is no mean pace.

Spain’s High Risk Election Process

As Mr Zapatero put it on Saturday, when he announced the date of Spain’s general election, the decision “is in the country’s interest” since from now on there will be certainty, and “certainty is stability”. While it is quite possible that almost all of Spain’s politicians shared this sentiment, and welcomed the bringing forward of the election date, they may very well be the only ones to do so. Certainty is undoubtedly a strong positive, but when the only thing about your country which people can be certain of is the election date, then maybe on balance you won’t have gained much. Continue reading

A Hungarian Waltz On The Wild Side

The Hungarian government’s much publicised unorthodox plans to cut the country’s public debt level has been attracting a lot of attention of late, both from the media and from the rating agencies. Some observers have been quite positively impressed. Fitch Ratings, for example, raised their outlook on Hungary’s sovereign credit rating in early June from negative to stable, citing government plans to reduce what is currently the largest accumulated public debt among the European Union’s eastern members. Others, however, continue to have their doubts. Moody’s, for example, has decided to maintain a negative outlook on the country’s due to concerns about the general trend in government policy, and the possibility of slippage with deficit objectives. Either way, these are changes within very defined margins, since at the end of the dat Fitch currently still rates Hungary at BBB- and Moody’s at Baa3, in both cases these ratings amount to the lowest investment grades. Continue reading

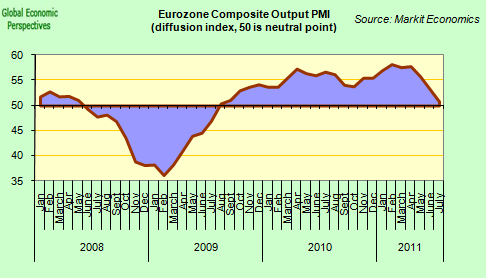

Recession Warning On Europe’s Periphery

As Europe’s leaders struggle to convince markets that their Greek debt problem-resolution-proposals are actually viable, and will really do the trick, last week’s flash PMI readings seem to have attracted rather less attention than they might. Nonetheless, the fact of the matter is that it is steadily becoming clearer that the current slowdown in Eurozone economic growth is turning into something more than just another one of those pesky “soft patchesâ€. The pace of economic expansion in core Europe has slowed dramatically, falling back in July for the third consecutive month, according to the latest flash PMI. Commenting on the flash results Chris Williamson, Chief Economist at Markit said: “The Eurozone recovery lost almost all of its momentum in July, recording the weakest growth since August 2009 when the recovery first began. Excluding the financial crisis, the July survey was the most downbeat since the Iraq war in 2003, and consistent with a flat trend in quarterly gross domestic product.

Simple and repellent: update

Does anyone else think the simple and repellent plan is getting a little traction? Certainly, more and more mentions of the idea of buying back tons of distressed Greek debt and therefore both reducing the total and converting it into a liability between Eurozone official institutions seem to be out there.

They better be: here’s a study into the effects of the crisis on European suicide rates.

Did Latvia really lose that much competitiveness???

Please think of this as a supplement and a slight challenge to Ed’s fine 23 May 2011 piece on Latvia. Besides giving us the most interesting (or weird? 🙂 ) title for a long while, he raises some very important questions: Is the Latvian internal devaluation really over and has it been successful? Ed is not convinced – neither am I but I am not as pessimistic as he seems to be. Continue reading