America, we know, has a currency union that works, and we know why it works: because it coincides with a nation — a nation with a big central government, a common language and a shared culture. Europe has none of these things, which from the beginning made the prospects of a single currency dubious.

Paul Krugman – Can Europe Be Saved?

All theory depends on assumptions which are not quite true. That is what makes it theory. The art of successful theorizing is to make the inevitable simplifying assumptions in such a way that the final results are not very sensitive.’ A “crucial” assumption is one on which the conclusions do depend sensitively, and it is important that crucial assumptions be reasonably realistic. When the results of a theory seem to flow specifically from a special crucial assumption, then if the assumption is dubious, the results are suspect.

Robert Solow, A Contribution To the Theory of Economic Growth, 1956

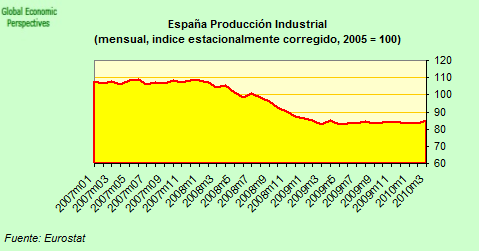

One of the key premises underpinning the establishment of the Euro as a common currency to be shared by a number of individual national states rather than one single nation was the central idea that the several economies of the participating countries would eventually converge to one common typology. That is to say, even if the individual nations would not be dissolved into one single superstate, then the idea was that the difficulty this could obviously create would be overcome by the generation of a number of different, but to all-important-economic-effects identical economies, each one a replica (in minature or “a lo grande”) of the other. Absent this, it is hard to see how people could have convinced themselves that having a single currency and a single monetary policy could possibly work in the longer term. Continue reading