Well, the latest batch of EU interim growth forecasts are out, and there are few surprises after so much prior comment. The Euro Area as a whole is expected to contract, but of course within the aggregate contraction some will fare rather better than others. “The EU is set to experience stagnating GDP this year, and the euro area will undergo a mild recession”, according to the press release. What this means in practice is that Greece is expected to contract by 4.3%, while the German economy is forecast to grow by 0.6%. During yet another year Eurozone economies are expected to diverge far more than they will converge. Downward revisions of one percentage point or more were made to the forecasts for Estonia, Spain, Greece, Italy, and the Netherlands, while those for Germany, France, Austria, Slovakia, Denmark, Poland and the UK were either left unchanged or reduced by less than a quarter percentage point. No one was revised upwards. Continue reading

Ireland’s small bazooka

The Wall Street Journal’s Marketbeat blog discusses an interesting flow chart prepared by BNP Â Paribas which shows the various scenarios that could play out following the imminent Greek bond offer to its private bondholders. Among the apparent paradoxes brought out by the chart is that Greece could be better off from a debt reduction perspective if a small majority rather than large majority of bondholders accept the offer, because then it will have the latitude to, er, screw the holdouts, including the possibility of giving them nothing. Whereas with a very high majority, there will be a strong incentive to keep everything consensual and the holdouts escape at par.

Anyway, the chart refers to the scenario where Greece is able to impose a punitive scheme on the holdouts as “Anglo Irish.” Â This is because of the bank’s 2010 offering to subordinated debt holders, who were offered new bonds with 20 percent of the face value of the old ones, and by accepting they were voting to impose essentially a complete wipeout of anyone who didn’t accept. FT Alphaville discussed the strategy in detail at the time.

It’s a perfectly good label, but if you come away from the chart thinking that Ireland came up with a hardball (or is that “fair shoulder”?) solution to its problem of bank debt, you’d be wrong. That particular offer only dealt with a tiny proportion of Anglo’s overall debt, and it was the easiest target. In fact, far larger public sums have been spent paying at par the legacy unsecured and unguaranteed senior debt in Anglo Irish — claims that would have only residual value had Anglo been allowed to go to the wall as an insolvent bank. Â The closer analogy is with the wheeze that the ECB just pulled to make sure its own holdings of Greek bonds get paid at par, despite having paid heavily discounted market prices for them.

So good luck to Greece with the Anglo Irish scenario. It would have been nice had it been tried on any larger scale in Ireland.

For Whom The Bailout Tolls

“On an optimistic view, that a deal was struck implies that neither side was ultimately willing to risk a Greek exit because they recognise that no one fully understands all the ramifications of such a decision. Under this scenario, when pressure again builds, the authorities will do the same: let Greece remain in the euro, even if it fails to keep to its adjustment programme. So, the reality of “bail-out II†means that, if the situation becomes critical, there will be a bail-out III”. Sushil Wadhwani, writing in the Financial Times

So Greece has finally been awarded a second bailout. One may wish the country will live to tell the tale. Continue reading

Stimulus? It’ll all go to China. Or not

This new post at VoxEU on the sudden plunge in world trade in 2008-2009 is very interesting. For one thing, it gives us some detail about how the crisis was transmitted around the world, and how this transmission happened between typically supply-side factors (wages are too high, the wrong goods are produced, everyone is suddenly a “zero marginal product worker”) and demand-side ones. It seems that the unprecedently large chunk of world trade that consists of intermediate goods in supply chains played an important part. On this occasion, “The World, On Time” was the last thing anyone wanted.

Another interesting and important point which isn’t explicitly made is that fiscal stimulus didn’t actually “leak” as so many people feared. Countries that carried out substantial stimulus didn’t see their balance of payments get sharply worse. This is because public spending often goes into nontradable goods, and the rest is often spent on home production.

In so far as you want “rebalancing”, then, it doesn’t make sense to think that austerity leads to it.

Quick Reality Czech

The Czech Republic is the first economy in central and eastern Europe to slide back into a full technical recession during the current downturn (evidently it is unlikely to be the last), with a 0.3 per cent quarter-on-quarter GDP decline in the last three months of 2011, after a 0.1 per cent drop in the previous quarter.

on buckets

I have an editorial up at Global Times on the Sun, Murdoch and media ownership generally. The story is from Horrie and Chippendale's Stick it Up Your Punter.

trying to find home

At the end of that war in 2006, I felt the cost of that more than I ever had. My marriage had fallen apart, I was away from my daughter, and I really didn't have a sense of having a home. And that was what was so important about being in Marjayoun and rebuilding the home. At its most elemental, it was about trying to find home, and in the end, I did.

From a very recent interview with the late Anthony Shadid, probably the best pure reporter of the 9/11 wars. Obituary here, along with an archive of his stories.

busty Dawn Raid says ‘i like it first thing’

But Kavanagh's lengthy column managed to avoid naming to the Sun's readers a potential offence among those being investigated – bribery of police officers.

Indeed. And I love the way the Guardian has stepped back from driving the hackgate revelations to keep the whole mery go round whirling with a few swift stiletto jabs. Anyway, as David Leigh makes clear it’s not a case of victims being treated like criminals, but of alleged criminals becoming victims of circumstances they did their best to help create. Item:

The Sun has always stood for the freedom of the entrepreneur to do as he sees fit with his own companies. What the entrepreneur sees fit to do in this case is to make an example of what he wishes others to believe is a rogue operation within his company.

The Sun has also been a tool for its parent company’s wider business interests, whether expressed through its political ‘reporting’, its relentless cross-promotion of Sky or its attacks on the bosses competitors. It is now in the interests of the wider business to serve the Sun up on a plate.

The Sun has always stood for robust policing. Until, apparently, it was applied to its own hacks. Additionally, the Sun likes spectacular policing, of the kind that provides good copy and that demonstrates Something Is Being Done. Something like a multiple dawn raid pile in, for instance.

The Sun has always believed in the American alliance. Now it’s finding out in microvcosm the truth of Bismarck’s remark that every alliance consists of two partners: a stronger one and a weaker one.

The actual circumstances of the raid on the Sun’s hacks may be up for debate. I think they’re pretty standard for today’s exciting world of high profile send a message coppering, but that may be because I’m a bit too used to living in the kind of authoritarian pro-business society that the Sun has always campaigned for. This is also why I’m a bit baffled by the people who seem to think that we’ll ‘lose something’ when it goes. 'What will remain' is the problem.

More generally, it does look like the Sun is done for. Apart from the fact that if the arrests continue its going to have difficulty getting out a paper there’s also the fact that no public official will want to talk to the paper right now: it makes them look dodgy. And those channels are what it needs to influence policy. Without them, it’s just a shit sheet like the Star.

waiting for the barbarians

Quite astonishing but nonethless entirely unsurprising piece on McKinsey's role in guiding, structuring and writing Lansley's NHS Bill. It's not so much regulatory capture here as regulatory conquest: the whole service is being chopped up and offered round its clients like a tray of hors d'oevres. It should be said that the company got a lot of its forward operators in place under the last government. That was the reconnaissance. Now, the assault.

What I'm not clear about is why Cameron's put his political credibility on the line, not for ideological or populist reasons, but to ensure McKinely's bottom line. I think there's a general subtext here in that when the economy enters a long depression, securing lines of revenue from the taxpayer becomes a more important profit strategy for business.

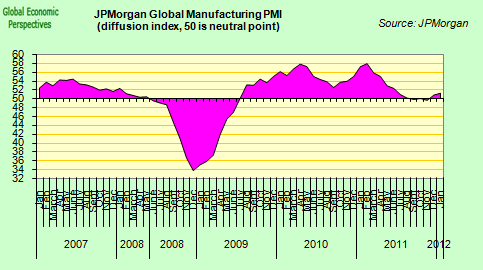

Global Manufacturing Steadies As She Goes, Or Does She?

The year got off on a much better foot than might have been expected, at least as far as global manufacturing is concerned. As the JP Morgan report puts it:

“The global manufacturing sector continued to record belowtrend growth at the start of 2012. At 51.2 in January, the JPMorgan Global Manufacturing PMIâ„¢ rose to a sevenmonth high, but remained below its long-run average (51.8). Manufacturing output expanded for the second successive month in January, as new orders rose for the first time since last August”.

“The cyclically sensitive new orders-to-inventory ratio also moved higher, reaching a ten-month peak. Although rates of expansion for both output and new orders were the fastest since last June, they were still only modest at best. Growth of production was recorded in the US, Japan, Germany, the UK, India, Eastern-Europe, the Netherlands, Austria, Canada, Switzerland, Turkey, Brazil, South Africa and Denmark”.

“International trade volumes improved for the first time in six months during January. Growth of new export orders was led by India, the US and Turkey. China, Japan and the UK all reported modest increases, in contrast to the declines seen in the Eurozone, Russia, Canada, South Korea, Taiwan and Brazil”.