As doubts grow that in the post Dubai world Russia’s central bank will be able to sustain a great deal of momentum in its ongoing programme of interest rate reductions, we learn this week that the pace of expansion in Russia’s economy slowed back in November, following two months of steady advance in September and October. This time services activity also weakened its advance while manufacturing activity registered its second month of contraction. Yet the central bank may well show increasing restraint in lowering interest rates, even as the economy slows, the ruble rises, and bank retail lending continues to fall, having declined for nine consecutive months up to and including October, while corporate lending dropped for a second month in a row and hasn’t risen for six months (for more on the particular topic see my recent post – Are Russia’s Consumers Getting “Carried Away” With Themselves?). Continue reading

Global Manufacturing Loses Momentum In November

Operating conditions in global manufacturing industry improved for the fifth successive month in November, although there was an evident slowdown in the overall rate of expansion, with differences between countries accentuating and not diminishing. The JPMorgan Global Manufacturing PMI aggregate reading came in at 53.6, down from October’s 39-month high of 54.4, and signalling that the first wave of post crisis momentum may be losing force as governments slowly start to remove stimulus measures.

Europe in the 2010 World Cup

Looks a lot like Europe in the 2006 World Cup, actually.

Qualifiers this time: Denmark, England, France, Germany, Greece, Italy, Netherlands, Portugal, Serbia, Slovakia, Slovenia, Spain and Switzerland. That’s almost the same list as last time. Oh, we won’t have Poland, or Croatia, and the Danes, Slovaks and Slovenes got in, but eight of the thirteen are the same, and the Big Five all got in as per normal. Is it cynical of me to think that switching the Slovenes and Greeks for Sweden and the Czechs won’t make much difference?

Anyway. Consider this an open thread for World Cup football. With 192 days to go, what have been the big surprises so far? (Have there been any, really?) And what are the wild hopes? Who’ve you got?

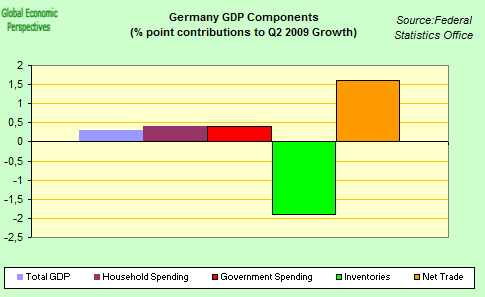

Is There A Double Dip Risk In Germany?

This is not an idle question. Despite all those bullish headlines in the press, most informed observers – including Bundesbank head Axel Weber – are only to well aware of just how fragile the German recovery actually is. Indeed only last week the OECD warned that Germany’s economy, may only recover slowly next since investment “is lagging,â€. The OECD now predict that German gross domestic product will expand 1.4 percent in 2010 and 1.9 percent in 2011 after shrinking 4.9 percent this year, which is in fact up on their earlier estimate, where the OECD predicted German growth of 0.2 percent next year. So whichever way you look at it, output at the end of 2010 will still be well down of 2008 levels. Worse, events like the recent upheaval in Dubai start to cast doubts on whether even the rather optimistic 1.4 percent growth level may now not be excessively optimistic for next year. The problem is that the recent rebound in Eurozone growth is extremely uneven as between countries, and, given its long standing export dependence, the German economy is hardly going to be leading the charge. As I said in my most recent post on the Eurozone :

“The question in hand is the Eurozone third quarter growth one, and the story is all about differences (between countries) and these differences in the key cases (France and Germany) are in many ways all about inventories……Now if you look at the chart below, you will see that German growth was in the second quarter was, more than anything, a statistical quirk which resulted from a balancing act between strong swings in inventories and in net trade. In the third quarter, as far as we can see (since we don’t have that ever so important detailed breakdown), this position has quite literally been inverted, as the earlier trade bonus has been eaten away by growth in imports (largely to stock up on export oriented inventories, not items destined towards domestic consumption) and this part we more or less know, since we do have all the trade data in for the quarter. ”

About that coal in Kosovo (II)

A couple of years back, I wrote an article about Kosovo’s coal industry. Short version: Kosovo has lots of coal, and most of it is middle-quality lignite. But the mines suffer from a horrible lack of investment; many of them are still using thirty to forty year old equipment. So both output and quality are far below where they should be.

So I wasn’t exactly surprised to see this recent article:

Total Eclipse At The Heart Of Dubai’s World

Back in the heady days of 2006 some 30,000 cranes, roughly a quarter of total global capacity, were busy whirring away in Dubai. Today most of these devices have either left to find service in other parts of the globe, or lie silent, unused and unloved. In what is only the latest sign of the ongoing property snarl-up affecting the emirate Nakheel, Dubai World’s property developer subsidiary, asked on Wednesday for a delay in their next debt payment. The move was widely seen by investors as a technical default, raising concerns about investment in risky assets right across the globe. So while their company slogan may well be that the sun never sets over Dubai World, the fact is that Dubai World’s sun not only no longer shines, it is suffering from something more like a total eclipse. Continue reading

Wasn’t Someone Else Involved?

An op-ed guest writer for the New York Times opines:

SIXTY-FIVE years ago, in November 1944, the war in Europe was at a stalemate. A resurgent Wehrmacht had halted the Allied armies along Germany’s borders after its headlong retreat across northern France following D-Day. From Holland to France, the front was static — yet thousands of Allied soldiers continued to die in futile battles to reach the Rhine River.

One Allied army, however, was still on the move.

Are Russia’s Consumers Getting “Carried Away” With Themselves?

“Cutting rates by 50 basis points here and there is not going really diminish the appeal of the ruble,†said Manik Narain, an emerging markets strategist at Standard Chartered Bank Plc in London. “In terms of nominal interest rates Russia (at 9% as of 24 November) is still offering the highest yields in the emerging market space and in an environment where oil prices are remaining relatively well supported we think that the ruble will continue to be seen as an attractive way to position for global recovery,â€

The world’s central banks are having a hard time of it these days, having just gotten through the worst banking and financial crisis in living memory they now face a growing dilema between continuing to give support to the developed economies (which are yet to recover from those early hammer blows) and the danger of creating fresh global asset price bubbles in emerging economies, asset bubbles which could easily be being fuelled by low US interest rates and a weak dollar. The latest warning in this respect comes not from Nouriel Roubini (or even from me, but see this post, and this recent interview I gave on Forex Blog), rather it emmanates from Germany’s new finance minister, Wolfgang Schäuble. His comments – which were cited in last Saturday’s Financial Times – highlight official concern in Europe that the exceptional steps taken by central banks and governments to combat the crisis carry with them a series of undesireable side effects. Continue reading

Ireland: The Reign of the Salaryman

There is something very traditional about the Irish economic crisis. If you consider the staples of 1980s economics, they were the ideas that nominal wages adjust very slowly downwards and that labour markets segment strongly into insiders who are able to hold onto jobs in recessions and outsiders who bear the burden of adjustment either through job loss or wage cuts. That’s a fairly accurate description of Ireland over the last year.

EU Lisbon jobs open thread

It’s now clear that the Thierry Henry assist on the William Gallas goal last night is going to generate more commentary and interest than tonight’s filling of the new EU jobs (Council President, High Rep. for Foreign Policy, and Secretary General of the Council), but nonetheless, we could be stuck with these people for a while so no harm in keeping track. What we know: Tony Blair is out of the running for Council President, but Catherine Ashton who arrived as Trade Commissioner in Mandy’s stead apparently on the inside track for the foreign policy job. They’re probably still having dinner at the summit and perhaps Irish PM Cowen has already cornered Sarko to argue Ireland’s case from last night, so there could a lot of distractions. But we’ll keep an eye on it.

UPDATE: Well, that was fast. Once Blair was out, the deal fell into place. Herman van Rompuy as Council President.  Almost as soon as Lisbon went live, the countries seem to be working to restrain its institutions.